|

For the past two years, I have been preaching to “listen to the Fed”. The Federal Reserve, the governmental agency tasked with “maximum employment and price stability”, has been steadily raising interest rates over the past two years. They last raised interest rates in July and then went on an expected pause to see how policy affected the high inflation rate they were attacking. Surprisingly, even as interest rates rose dramatically, the pace of companies hiring slowed only marginally and has remained over 200,000 new jobs per month through the November jobs report. This was in stark contrast to the widespread expectation for a recession following the dramatic interest rate hikes.

The big story of this past quarter occurred in mid-December at the last Fed meeting of the year. As was widely expected, the Fed held interest rates unchanged. However, the two big surprises came from the notes to their two-day meeting and Jay Powell’s press conference at the end of the meeting. In the notes, the Fed governors indicated they expected up to three interest rate cuts in 2024 which was a shock. Many investors had assumed one or maybe two interest rate cuts with those coming later in the year. I was in that camp, as the Fed has been consistently saying “higher for longer” meaning they want to keep interest rates at higher levels until the inflation rate returns to their 2% target range. In a bigger surprise – at least to me – Jay Powell stated in the press conference in response to a question about the timing of the rate cuts that he would expect to cut rates before inflation hits the 2% rate in order to not overshoot the target. With inflation currently around the 3.1% level, this opens up the possibility of a first rate cut in the first half of the year. With the probability of interest rate cuts on the horizon, this means a shift in investing. As interest rates fall, small and midsized companies should do better. Also, more growth-oriented companies such as tech companies should do better as interest rates fall. Given this Fed pivot, you can expect some changes to our investment lineup. Some of the changes are already in place while others will be coming soon. We have been watching a number of smaller and mid-sized companies as solid investment opportunities, but many of these stocks have seen a large run-up in price in recent weeks leading to them being “over bought” for now. We would expect prices to correct a bit, as they have been doing in the past few days, giving us a better buying opportunity. In addition to adding more smaller and mid-sized companies to client portfolios, we will be moving to more growth-oriented mutual funds for clients as well as adjusting our fixed income (bond) holdings to take advantage of the potential rate cuts to come. In finance-speak, we are going to extend the duration of our fixed income holdings. To explain that in plain English, we will be selling bond funds that focus on short-term bonds and adding funds that hold bonds that mature further out in time. This will take advantage of locking in these higher interest rates, and we should see some gains in value as interest rates fall, which will increase the value of the bonds in these funds. This past quarter, we made a few trades. We bought a U.S. Treasury note when interest rates were very near their peak, locking in a 5.2% yield through the August 2025 maturity. We also started adding a few selective smaller and mid-sized companies to client portfolios. One company that we picked up at a very reasonable valuation is egg producer Cal Maine Foods Inc. (ticker: CALM) which is already up 14% for us. Another small but growing company we added is Wabash National Corp. (ticker: WNC) which builds semi-trailers, truck bodies (think of box trucks) and processing equipment. This is a classic industrial company that is in very good shape and growing at a nice rate. Just before year-end we added a new bond fund to client accounts. We added the Janus Henderson Mortgage-Backed Securities ETF (ticker: JMBS) across most client accounts. This fund invests in mortgage bonds and, more specifically, mortgages that are backed by governmental agencies such as Federal National Mortgage Association (“Fannie Mae”) or the Government National Mortgage Association (“Ginnie Mae”). This government backing provides a level of stability to the bond holdings in the fund. Another new investment is the Putnam BDC Income ETF (ticker: PBDC), which invests in business development companies (BDCs). These are investment companies that primarily make loans to small but growing businesses that are not large enough to go public yet and need capital to grow. Sometimes, these BDCs will also take an equity stake in these businesses. These investments are a bit riskier, but often provide higher returns to investors. On the flip side, we sold our investment in online file storage company Dropbox Inc. (ticker: DBX) for a little more than a 15% gain in five months. We also sold out of Expedia Group Inc. (ticker: EXPE) – too soon it seems – for a small 3% gain. The financials seemed to be deteriorating so we chose to seek investments with a better margin of safety. Another sale was the SPDR S&P Oil & Gas Exploration & Production ETF (ticker: XOP). This had been doing well, but oil prices have been falling steadily since their late-September peak. We managed to book about an 8% gain on this fund. We also eliminated our holding in the WisdomTree Floating Rate Treasury ETF (ticker: USFR) as this was part of our shift from funds that focus on short-term bonds to ones that focus on longer-term bonds. Overall, we had a productive quarter and a very productive year. Client account returns were very good across the board. While I am very pleased, I am working to improve client performance without taking additional risk. By selectively using some option strategies, we should be able to continue to enhance client returns over time. As always, we truly appreciate the trust you have placed in us, and the opportunity you have given us to manage a portion of your assets. If you have any questions or need to discuss any issues, please feel free to give us a call. Sincerely, Alan R. Myers, CFA President / Senior Portfolio Manager Aerie Capital Management, LLC (866) 857-4095 www.aeriecapitalmgmt.com

0 Comments

This seems to have been the quarter when investors finally started to believe what the Federal Reserve has been saying for the past year and a half. Ever since the Fed started raising interest rates in early 2022, the mantra has been “raise interest rates to the target goal to choke off inflation and keep rates at that level until the goal is met.” That clearly stated goal didn’t prevent many market pundits from predicting interest rate cuts as early as the fourth quarter of this year.

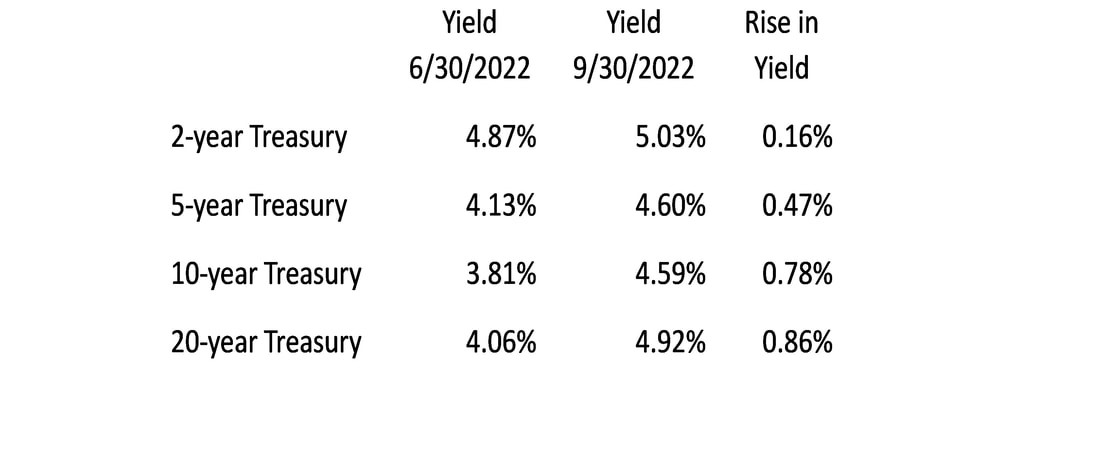

What caused the shift in perspective? Simply put, economic data continued to be relatively strong. The continued solid economic numbers – from job growth to wages modestly increasing – have served to keep the pressure on the Federal Reserve in their inflation battle. While the inflation rate has dropped significantly from 9.06% in June 2022 to around 3.67% as of August, we are still not near the 2% target rate the Federal Reserve has set. As investors reassessed the big economic picture, we saw interest rates – especially longer-term interest rates – rise relatively dramatically, which caused stock prices to drop for the quarter. As you can see by the table below, interest rates moved up across the spectrum. In fact, with interest rates on Treasury bonds at highs we have not seen since 2006, we are actively looking at a few bond ideas for clients to lock in some of these higher rates. If our thesis is correct – that interest rates will remain at these elevated levels for at least the next year before we start to see any cuts in interest rates, we can earn 5 – 5.5% in interest and we may be able to see some capital gains from any individual bond or bond mutual funds we hold. These higher interest rates led to lower stock prices. The S&P 500 Index – heavily influenced by seven very large tech companies that were viewed as “safe havens” for institutional investors – fell 3.65% for the quarter. A better measure of how stocks in general fared is the equal-weight version of this index, which fell 5.45% for the quarter. The reason stock prices fell is that when investors have a choice between a higher, safer return (bonds) versus a potentially high but riskier return (stocks), they will usually choose the more certain investment option. In the current environment, when investors see a relatively sure 5% return from Treasury bonds or 6 – 8% potential return from riskier stocks with a lot more volatility, the safer return becomes the more attractive option. While stocks in general fell, not all sectors did poorly. The energy sector (oil and gas) did very well, with the S&P 500 energy sector gaining just over 12% for the quarter. The exchange-traded fund we hold across multiple client accounts, the SPDR Oil & Gas Exploration & Production ETF (ticker: XOP) gained 15.49% for the quarter. This resulted from oil rising from $70 per barrel to around $90 per barrel at the end of the quarter. Oil has pulled back a bit in price since the end of the quarter, but we continue to believe the long-term trend is for oil to remain in this price range. In part we were not very active traders this past quarter, adding only one new position in travel website company Expedia Group Inc. (ticker: EXPE). While the stock is down from our original purchase price, we still feel the company is very undervalued. We also added to our position in the VanEck Morningstar Wide Moat ETF (ticker: MOAT) several times as the price pulled back throughout the quarter. This mutual fund has been one of the best performing funds investing across large capitalization companies. This fund is now about 10% of a typical client account allocation so we are satisfied with that level of investment. Our outlook for the year ahead is the same as it always has been – believe the Federal Reserve. They have stated their intentions very clearly, and they have followed through on them. Interest rates are likely to remain around the current levels for the next few months. My one fear is that the Fed becomes too laser-focused on a 2% inflation rate. Our economy faces some structural changes – the baby boomers are retiring in droves and there are not enough workers behind them to take their places – so targeting a 2% inflation rate as we had over the past decade may not be realistic. Targeting a range of 2% - 3% inflation is probably more feasible and sustainable, but we will have to see how things evolve. As always, we truly appreciate the trust you have placed in us, and the opportunity you have given us to manage a portion of your assets. If you have any questions or need to discuss any issues, please feel free to give us a call. Sincerely, Alan R. Myers, CFA President / Senior Portfolio Manager Aerie Capital Management, LLC (866) 857-4095 www.aeriecapitalmgmt.com |

RSS Feed

RSS Feed

Contact us

|

|

© COPYRIGHT 2015. ALL RIGHTS RESERVED.

|