The big news in the world of investing is how “the market” has recovered everything it lost and more, closing at a new all-time high yesterday. Before we all run out to celebrate, let us back up half a step and look at the reality versus the hype. As you know, I have been saying that there are really two “markets” with the one in the news being a bit misleading. Allow me to dive into the weeds for a moment as a quick review.

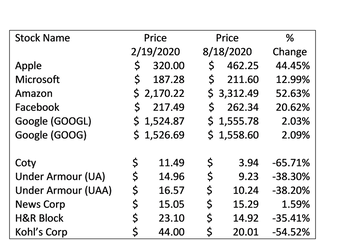

When most financial news media refer to “the market” they are referring to the S&P 500 Index. This is an index of 505 company stocks. This odd number is because there are a few companies that have two different classes of stock such as Alphabet (GOOG and GOOGL) or Berkshire Hathaway (BRKA and BRKB) and both are counted. The way the S&P 500 Index is calculated is to take the number of shares that are outstanding for a company and multiply that by the price the stock is trading at for the day. You then add up all of these market capitalizations, or ‘market caps’ for short, and compare it to the total market cap from yesterday. Currently, the total market cap for the entire index is around $24.4 trillion but the actual index value is about 3,389.78 as of Tuesday’s record close. The actual index value is computed by dividing this total market capitalization for all companies by a divisor number. This index is what we call ‘market cap weighted’ which means that companies that have a larger market capitalization have a much greater influence on the value of the index. Currently, Apple makes up almost 7% of the index, Microsoft almost 6%, Amazon 5% and Facebook 4% of the index’s value. The top 10 stocks – out of 500 names – account for almost a third of the index’s total value! What this means is these companies can have an outsized influence on the index’s performance. Suppose that, instead of using each company’s market capitalization to weight the index, we weighted each one equally. That is, suppose that one share of Apple counted the same as one share of Under Armour or Kohl’s or H&R Block, three of the smallest companies in the index. There is an exchange-traded mutual fund that does exactly that. And we can compare the returns of the market cap weighted S&P 500 ETF (ticker: SPY) to the equal-weighted S&P 500 ETF (ticker: RSP) to see why we shouldn’t necessarily be excited by the new ‘record’ in the index. As you probably know, the S&P 500 peaked on February 19 at 3,386.15 before the economy shut down for the pandemic and the index plunged to its low of 2,237.40 in March. Fast forward to now where the index closed at 3,389.78 for a new all-time high on Tuesday. Quite a run. But let us look at the equal weight index. Using the exchange traded fund, this index peaked a week before the market cap weighted index at a price of 118.71 per share. This ETF bottomed out at a yearly low of $71.66 in March. As of now, the equal-weight ETF is back to $110.39, which is still 7% below its former peak. Another way we can look at this is to look at the performance of the five largest holdings in the index and the five smallest holdings over the period from February 19 (the former peak) to August 18 (the new peak) to see how these stocks have performed. As you can see in the accompanying table, the stocks at the top of the index have done remarkably well while those at the bottom are still down significantly. In fact, 195 of the 500 stocks in the index are still priced below where they closed on February 19, prior to the tumultuous drop in price. What does this mean for the markets and for us as investors? One key is that just because “the market” has hit new highs do not assume the entire market has hit new highs. It is a very narrow group of stocks driving this index. This means there are still plenty of opportunities out there as these “secondary” stocks try to catch up to the much bigger names. However, I do not expect many of these names – think airlines, cruise ships, restaurants, and retailers – to fully recover until we have a widely available vaccine for the coronavirus. Now that we have hit new highs, I know the worry is going to be “is a decline right around the corner?”. While that is certainly a possibility, frankly I am not worried. Why? Largely because of the Federal Reserve. Why does the Federal Reserve matter? Money. The Federal Reserve is charged with maintaining stable prices in the economy (i.e. controlling inflation) and helping maintain full employment. Normally, the Federal Reserves uses a couple of tools for this. One is an ability to influence interest rates. Lower interest rates spurs more borrowing and spending and higher interest rates results in more saving and less spending. The other method of influence is by buying or selling bonds. Normally, the Fed buys Treasury bonds. During the latter stages of the Great Recession, when growth was still a very anemic 2% annually, the Fed stepped up to buy municipal bonds in addition to Treasury bonds. This was a bit unprecedented but designed to pump more money into the economy in the hope businesses would reinvest back into new property, plants, and equipment. Fast forward to this pandemic. The day the market hit its lowest point, the Fed announced a plan to pump $1 trillion in short-term cash loans to banks and to expand a $60 billion buyback of bonds. The following day, the market started its turnaround. Essentially, the Federal Reserve had become a “backstop” for the market. Fed Chair Jerome Powell has stated he will do whatever it takes (i.e. spend as much as needed) to “stabilize the markets”. While the Fed is never supposed to take its cues from the stock market, in many ways, that is exactly what they are doing. My expectation is that should we see the start of a market pullback, we will see the Federal Reserve step up and commit more dollars in more ways. They have already stepped up in ways that were unthinkable a few years ago. Over the past three months, the Federal Reserve has purchased not only Treasury bonds and municipal bonds but corporate bonds and bond ETFs (exchange-traded mutual funds). This is unprecedented but shows just how far the Fed will go to pump money into the economic system. How does that benefit us as shareholders? Given the current investing environment – interest rates at or near historic lows – the stock market is really the only game in town for any kind of a return. The Fed wants people to “feel” richer in hopes they will continue to spend money. They hope this “wealth effect” will sustain the economy on some basic level. So, anything to help bolster the markets will go a long way towards keeping the economy from sliding into a deep depression. Or so the thinking goes. The money the Fed is returning to the economy is simply flowing into the stock market. Any dips in the market are likely to be short-term in nature and offer buying opportunities for now. This is why I am not particularly worried about a major market pullback. At least, not while Jerome Powell is still Fed chair.

0 Comments

|

RSS Feed

RSS Feed

Contact us

|

|

© COPYRIGHT 2015. ALL RIGHTS RESERVED.

|